In the severe economic, social, and scientific turbulence churning at the dawn of the twentieth century, people were eager for any semblance of stability and predictability. From this need for certainty emerged a group of entrepreneurs who promised to apply scientific methods to predict the economic future, and in essence moderate the risk of investing in capitalistic ventures.

“Forecasters found a ready audience during a time of social and economic turbulence”

In his book Fortune Tellers: The Story of America's First Economic Forecasters, Harvard Business School's Walter A. Friedman chronicles a host of academics, businessmen and, yes, charlatans who ultimately failed to foresee the biggest economic event of the twentieth century: The Great Depression.

In an e-mail interview, Friedman, director of the HBS Business History Initiative, discusses his book and the uncertain times that underscored the risk and uncertainty inherent to capitalism itself.

Sean Silverthorne: Why did you decide to write this book?

Walter Friedman: The idea came to me years ago when teaching "Creating Modern Capitalism," a short course that was once required for incoming MBA students. Tom McCraw, the architect of the course, emphasized the idea that capitalists could be defined as people who "put bets on the future"—by, for instance, making investments, opening sales campaigns, and founding new firms.

The subject of forecasting, I decided, would allow me to explore this idea. How do people predict the economic future? How have forecasting methods changed over time? What makes one forecaster more popular than another? I chose to research these questions by focusing on the first generation of economic forecasters—those who founded their agencies in the early twentieth century. Forecasting is such a deeply entrenched and ubiquitous activity today that I thought it would be interesting to see how it got started. How did a world of astrology and "sign-reading" turn to one of econometrics and leading indicators?

Q: Why did the group of pioneering forecasters that you chronicle enjoy so much success with clients and the public? What need were the forecasters fulfilling?

A: The key was the nature of the time. Forecasters found a ready audience during a time of social and economic turbulence. The late nineteenth and early twentieth centuries were a period of severe panics—in 1873, 1893, 1907, and 1920—and also a time of substantial demographic change, as the country moved from being predominantly agricultural to being industrial and urban.

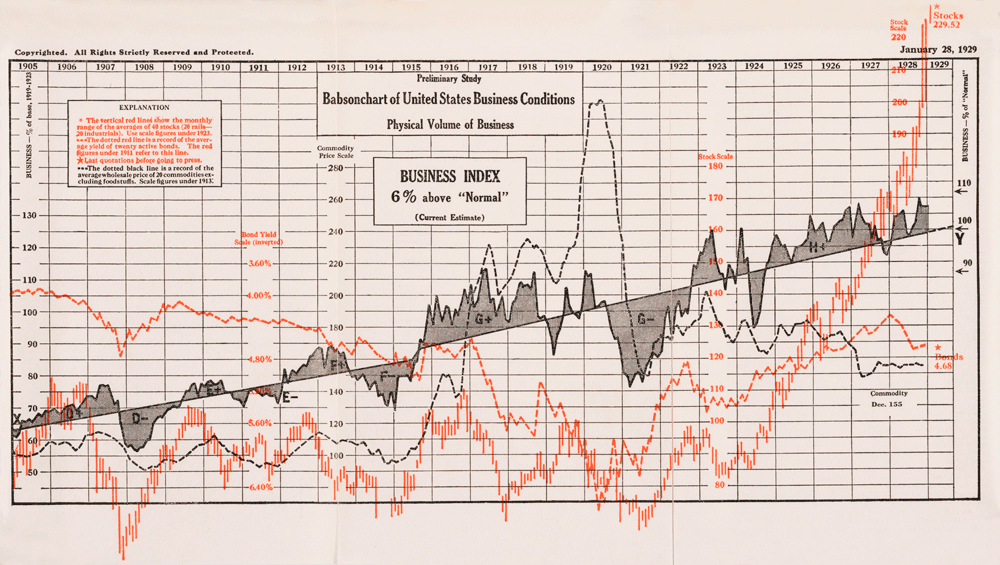

Babsonchart of United States Business Conditions," January 28, 1929, from Roger W. Babson.

Babsonchart of United States Business Conditions," January 28, 1929, from Roger W. Babson.For those who had suffered through financial panics, forecasting offered the idea that economic activity was not simply random, but followed discernable patterns that could be predicted. In a country whose population was moving from agriculture to industry, "business barometers" created the comforting idea that business activity was cyclical in the way that the weather was cyclical with changing seasons. Even the vocabulary of "barometers" and "cycles" was carried over from meteorology to economic prediction. Forecasting, through the use of statistics and economic charts, provided a sort of Farmer's Almanac for the industrial economy. It provided comfort as well as predictions.

Q: Has the business of forecasting proven to be lucrative?

A; Forecasting was a lucrative business for many of the pioneering forecasters. Roger Babson built a business empire around his weekly forecasts—an empire that included his newsletters, syndicated columns, and eventually a radio program. In 1919 he founded Babson College, today a highly respected institution, to provide him with a pool of workers for his forecasting business. Others, like Irving Fisher, were successful as forecasters in the 1920s but lost everything after the 1929 crash—an event he failed to predict. But, more generally, while individual forecasters came and went, some making it rich and others not, the bigger story is that the industry created key resources for society as a whole.

In the process of trying to make reliable forecasts, economists and entrepreneurs developed index numbers, leading indicators, and new economic charts, and even founded important institutions like the National Bureau of Economic Research. The economist Wesley Mitchell, who was deeply engaged with forecasting in the 1910s and 1920s, served as director at NBER for many years. One of his students, Simon Kuznets, developed [a standard way to measure] Gross National Product there in the 1930s. In all these ways, the growth of the forecasting industry spurred efforts to make sense of economic change.

Q: How has government's role in forecasting and data-gathering evolved in the US?

A: When forecasting got started, in the early twentieth century, there was little idea that government could or should play a role in stabilizing economic growth. Most people, like Babson, James Brookmire, and the Harvard economists C. J. Bullock and Warren Persons believed that the economy was simply too vast to be controlled in any meaningful way. Others thought differently—including Mitchell and Herbert Hoover. Hoover, who was Secretary of Commerce from 1921 to 1928 (when he began his successful campaign to become president), thought government could play an important role in controlling economic panics by providing objective (i.e. non-commercially biased) predictions of the economic climate. If businesspeople knew of economic conditions six months ahead, he reasoned, they could enact countercyclical policies that would temper any ups and downs. For Hoover, the government would, therefore, help to increase economic efficiency simply by improving the flow of economic information.

This view, in which government agencies could promote economic stability by providing forecasts, was a far cry from the type of direct involvement initiated by Franklin Delano Roosevelt in the New Deal. Still, it was an important stepping-stone from the previous generation who did not fathom a role for government in modifying the business cycle at all.

Q: What effect did the Great Depression have on the prediction business?

A: By the time of the Great Depression, several methods of forecasting had become popular. Many of them, including that advocated by Babson and by the Harvard Economic Society, perceived that the economy was best understood by studying recurrent historical patterns or past analogies. They promoted, each in their different way, the idea that economies were like atmospheres—independent, autonomous, and cyclical. But during the Depression, those forecasters who advocated that economies operated according to boom-bust cycles were left stranded. There was plenty of "bust" but there was no "boom" forthcoming. During these years, those people who advocated, instead, that economic activity could be greatly affected by policy gained prestige. Thus, even while Fisher sunk into poverty, his econometric ideas were gaining strength. Of course, the most popular economist of the 1930s became John Maynard Keynes, who similarly advocated that governments could, and should, intervene to control economic fluctuations when economies got stuck in a suboptimal rut. In decades after World War II, econometric and policy-oriented forecasting came to dominate the field.

Q: What are you working on next?

A: I have started a new book on the rise of big business in the twentieth century and its effect on American life. How did we become a nation of "organization men" in the 1950s, to take a term from William H. Whyte? How did that change pathways to success and ideas about citizenship? How did other countries perceive the rise of giant corporations in the United States?

As part of this project, I have been studying the history of Junior Achievement, which was a group founded in 1919 by AT&T president Theodore Vail, Strathmore Paper Co. president Horace Moses, and Senator Murray Crane (R-Mass.). Vail feared that the economic values were lagging among the younger generation of the time and he sought to reverse that trend. He set up a program for successful executives to educate children on the realities of economic life. Today, it is a thriving organization—one that reached 4.4 million US students just last year.

- Hugh Quick

- home, none

During my business career I came across a very capable 'planner' who pointed out that if you made forecasts of directly of what people wanted to know, e,g. next years sales the result was always wrong. However, by looking at the factors that went into making such a forecast some useful information could be discovered. For instance if you were selling widgets of a kind that people only wanted one, the number of people without one was useful information. It didn't tell you how many would be sold but it did tell you that it could not be more than 10,000 for instance. He promoted the idea of developing 'scenarios' for the future rather than specific forecasts, thereby saving the company from some costly mistakes.- Mervyn Extavour

- Director/President/Consultant, ACTT/NATPETT/NSP Consultants Inc.

Forecasting in economic terms has always been a challenging sphere for business persons as well as economists - for fear that they may not hit the target or that their prediction may be cause their downfall or make them unpopular.The growth of industrialization and the uncertainty of the 21st century, against the background of the financial fallout, coupled with technological advance, with a volatile marketplace does not make forecasting any easier.

However, the reference to Junior Achievement can be configured into a system that tells us our growth in the future of potential entrepreneurs for any society. But this must be coupled with close monitoring and the marshaling of investments in certain specific areas of economic activity. My experience with school students in Junior Achievement coupled with my lecturing activities has increased my passion for innovative ways to ascertain how the future will turn out for our business persons.

Statistics by themselves may tell a story or give a pattern, but the ability to foretell or forecast the future intelligently or accurately remains a huge challenge.

- Ryan Hunter

- Chairman's Fellow, Towers Watson

Walter: Captivating reflection on the thinkers and heretics who were driven to prove future economic events could be predicted.After your forthcoming work on the Rise of Big Business, it would be fascinating to continue the series by investigating The Cumulative Impact and Evolution of Small Business in the United States of America.

A few data points from the U.S. SBA:

1. The 23 million small businesses in America account for 54% of all U.S. sales.

2. Small businesses provide 55% of all jobs and 66% of all net new jobs since the 1970s.

3. The 600,000 plus franchised small businesses in the U.S. account for 40% of all retail sales and provide jobs for some 8 million people.

4. The small business sector in America occupies 30-50% of all commercial space, an estimated 20-34 billion square feet.

5. Furthermore, the small business sector is growing rapidly. While corporate America has been "downsizing", the rate of small business "start-ups" has grown, and the rate for small business failures has declined.

6. The number of small businesses in the United States has increased 49% since 1982.

7. Since 1990, as big business eliminated 4 million jobs, small businesses added 8 million new jobs.

Source: U.S. SBA http://www.sba.gov/content/small-business-trends

Then, after analyzing how small business is shaping today's economy and society, it would be particularly fun to hypothesize what's ahead for U.S. business.

Thank you for inspiring our thoughts and ideas.

- Kapil Kumar Sopory

- Company Secretary, SMEC(India) Private Limited

People - particularly those in distress - are prone to rush to astrologers who forecast the future based on certain parameters, knowledge of which they have acquired from here and there. Then comes the forecaster's intuition. As with the law of probability ( mathematically) so with the art of forecasting. However, the forecasting of economic indicators , even though professed to be based on adequate statistics, is somewhat clumsy as many factors, political for example, come to the fore and these lead to less chances of right predictibility.Forecasters generally thrive due to the human fraility of trying to save by catching a straw while almost drowning. They are clever to catch their 'prey' and play a game of somehow convincing the subject. They are very guarded in their reportings and use language/expressions which could have double (opposite) meaning so that they have a defence when the predictions fail.

We need to be guarded in outright and completely trusting even when the forecasters indicate that they are using tools of science to predict the future which, let us know, is being done solely with the aim of profiting from the forecasts.

A parallel to forecasting is very long-term planning. Even five year plans have the dubious distinction of little success and hence strategic planning works better.

In nutshell, we would be safer if we go to forecasters with caution and duly assess what is being told to us.

- Lori Jewett

- undergraduate, Oswego University

Is there a way to predict what our future economic growth for our livelyhood in regards to Industry, mining, agriculture will be since, most industries have moved out of the United States and agriculture in Northern New York is nothing like it was in the past. Also, what about the coal and mining in the United States? It is my understanding through history everyone that had land and planted needed to replenish the nutrients in the area they were growning crops. I am just wondering what we have here in the United States that we can rely on trading and supporting our Constitution. We seem to have so many laws governing other laws and so forth that the basics were lost in the process.